This is Why I Don't Use BRAVE Browser

Today was the concluding day for the group of 20 member nations' G20 meet in Japan. At the end of this two day summit, all leaders adopted a joint declaration and pledged for the full, effective and swift implementation of FATF Standards along with commitment to fight terrorist-financing, money laundering, corruption, bribery etc.

Indian crypto community is delighted to think that it brings some ray of hope for regulation of cryptocurrencies in the country. Among other things, FATF had proposed some strict regulatory recommendations for all crypto entities including crpto-exchanges, crypto asset managing companies etc. to collect and share KYC information with every transaction among themselves and with governments.

However, cryptocurrencies make a small part of this declaration. In fact, FATF doesn't even use the word cryptocurrencies but use the term 'virtual assets' instead. As per their proposal:

The FATF uses the term “virtual assets” to refer to digital representations of value that can be digitally traded or transferred and can be used for payment or investment purposes, encompassing both convertible and non-convertible, centralised and decentralised forms, as well as Initial Coin Offerings. This includes but is broader than crypto-assets, as they are commonly referred to by the G20.

So the focus is on broader terms like virtual assets, digitization and new technology.

PM Narendra Modi already champions the cause for anti-money laundering, black money, and corruption. He had also launched mission Digital India in the past for mass adoption of digitalization in the country. So I think, the government will interpret the declaration to imply to align with their own policy and intentions.

At G20, Indian Prime Minister has laid a great emphasis on collaboration among G20 nations to apprehend fugitives of financial crimes and perpetrators of economic offences, to strictly monitor money laundering activities and terrorist financing.

Indian government also perceives cryptocurrencies as a vehicle to facilitate money laundering, terrorist financing, protecting black money, running ponzi schemes, conducting financial frauds & misconducts and to indulge in illicit trades.

So India declined to be a signatory to the Osaka Declaration on digital economy proposed by Japan.

According to Japan, framing rules on data flow and e-commerce are the growth engine of digital economy and is an urgent mission.

Osaka Track was signed by 24 countries. It was originally intended to be part of main G20 summit but strong resistance from India forced Japan to put it in a secondary event.

Countries like US, Russia and China have supported Osaka Track. US even said that free flow of data is an integral part of digital economy's success in their country.

Thus India isn't influenced by what other developed and powerful economies of the world are doing. It likes to do things on its own way. So the argument that many countries are already regulating or planning for the regulation of cryptocurrencies doesn't make any sense in India.

Let Indian government do whatever it wants to do. But I'm sure that it won't be able to beat the smart Indian crypto community and they will always find the way to do what they want to do!

No government can strangle crypto. But it can be other way round!

This is Why I Don't Use BRAVE Browser

Bittrex Silently Re-opens STEEM Wallet

India wants to ban Crypto again. The sword of Damocles keep dangling indefinitely

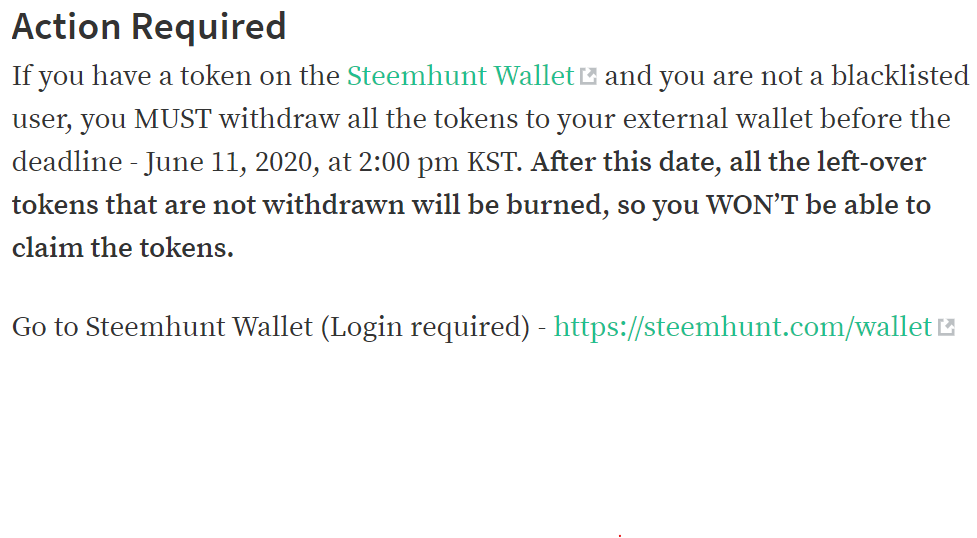

Withdraw Your $HUNT From SteemHunt Wallet. Else, They're Gone Forever!

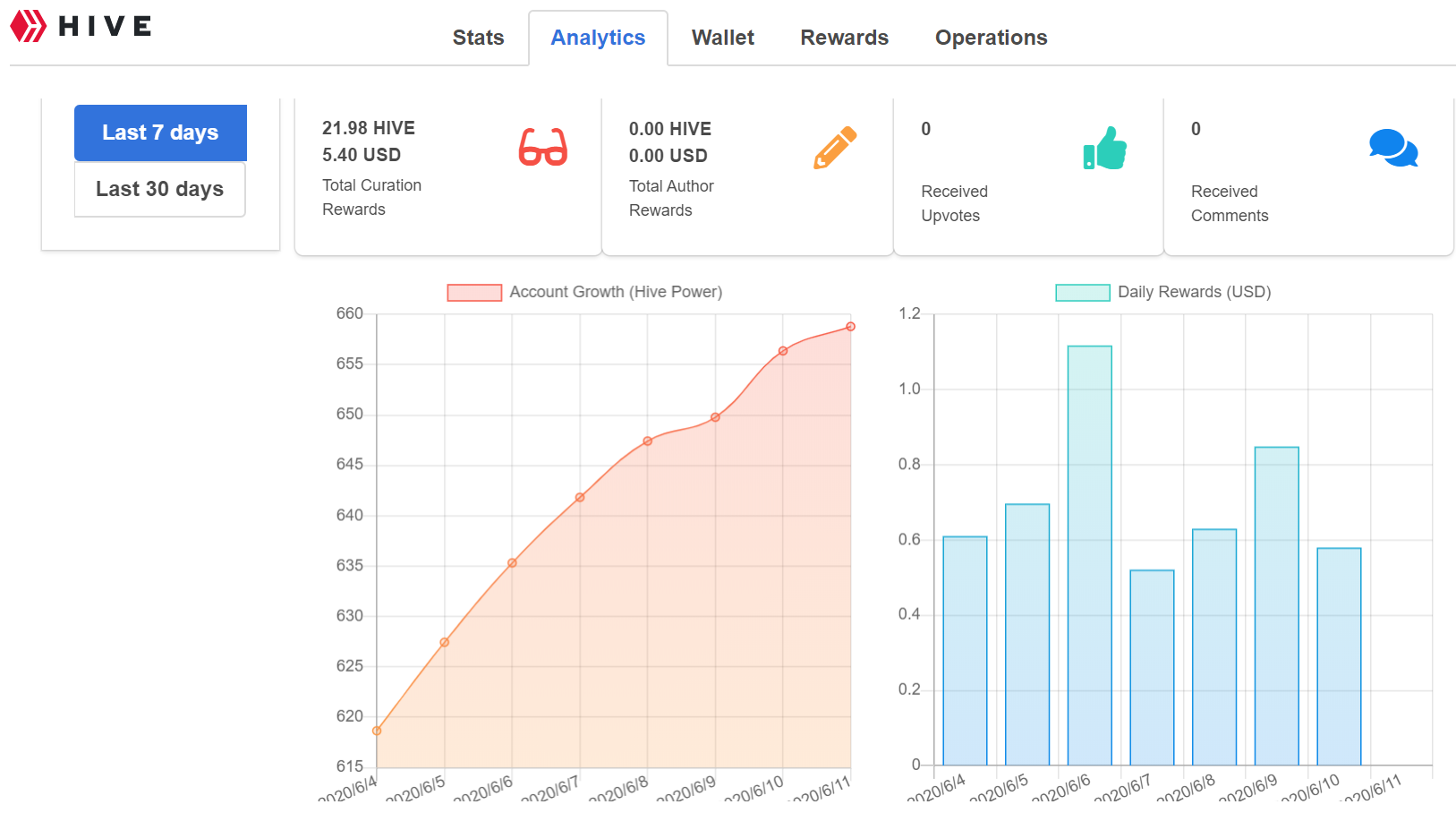

Earning by doing nothing - how much are you earning?

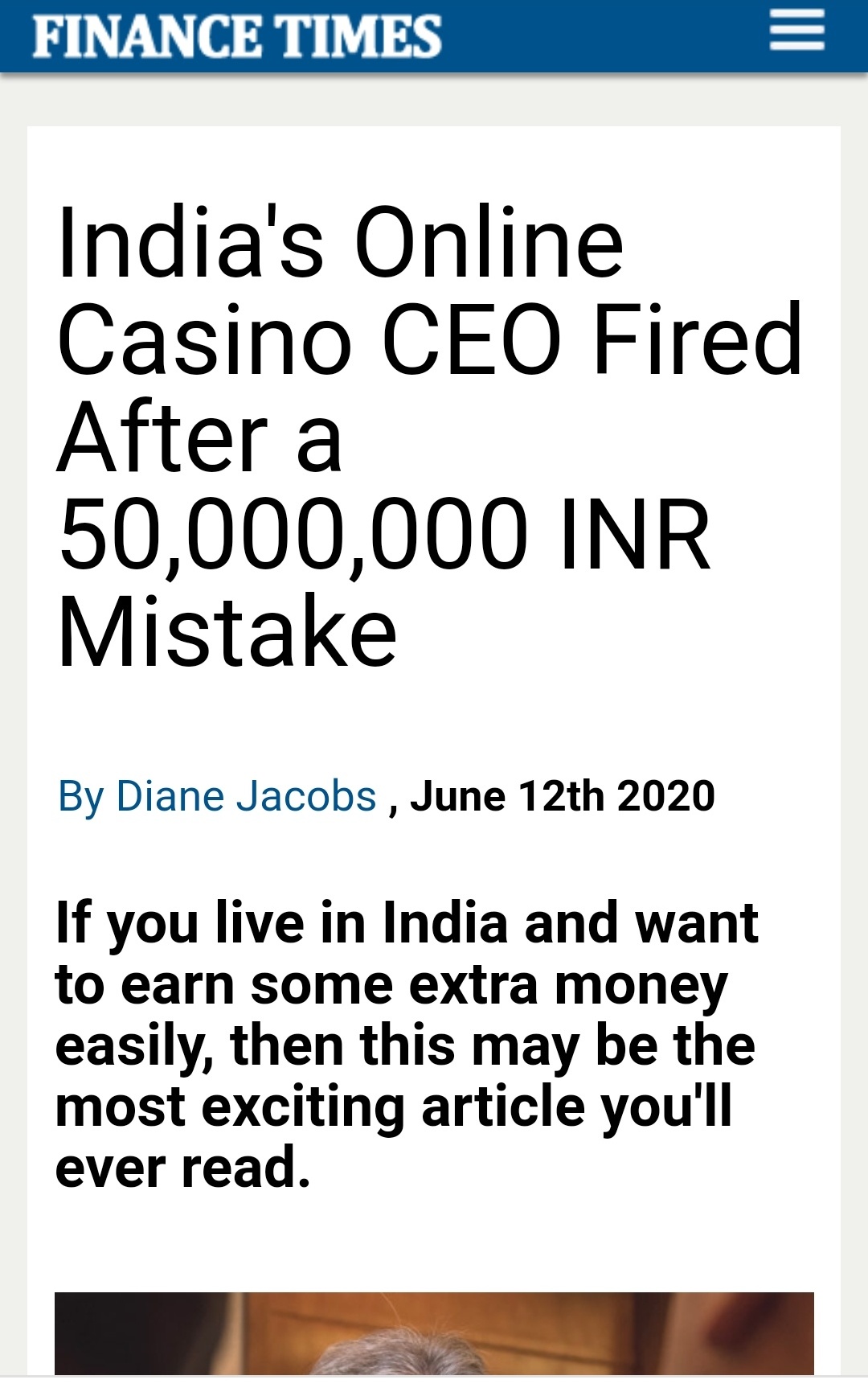

Is This Casino Being Scammed by Indian Users?

Was CoinDCX Security Compromised? Indian Crypto Exchange Finally Bows Down to the Twitter Pressure

What's Safer - Non- custodial STEEM Blockchain Wallet or a Custodial Wallet?

Wanna Double Your Money in 3 days. No ponzi! Real Deal.

विश्व पर्यावरण दिवस के मायने